Construction Loans Explained: What You Need to Know Before You Build

Building a custom home is exciting, but financing the process can feel unfamiliar if you’ve never built before. Many buyers don’t realize that applying for a new home construction loan is very different from getting a traditional mortgage. Unlike a traditional mortgage, a construction loan funds your home in stages throughout the building process. Understanding how construction financing works early can help you avoid delays, unexpected costs, and unnecessary stress.

For many buyers throughout Virginia and Northern North Carolina, the construction loan process is one of the biggest unknowns in the homebuilding journey. They have questions about down payments, draw schedules, interest rates, land ownership, and lender requirements.

At Rock River Homes, we help buyers navigate this process every day. For qualifying buyers, Rock River Homes may be able to simplify the process by handling the construction financing directly. This can reduce paperwork, minimize delays, and create a smoother path from land purchase to move-in day.

What is a construction loan?

A construction loan is a short-term loan used to finance the building of a home that releases funds gradually as construction milestones are completed.

This process protects both the lender and the buyer by ensuring funds are distributed as work progresses throughout the build.

Most construction loans:

- Last approximately 6–12 months during the construction phase

- Release funds in phases called “draws”

- Require inspections before funds are released

- Transition into a traditional mortgage after construction is complete, depending on the loan type

Construction Loan vs. Mortgage: What's the difference?

While both construction loans and traditional mortgages help buyers finance a home, they work very differently.

A traditional mortgage is used to purchase a home that already exists. The lender provides the full loan amount at closing, and buyers begin making regular mortgage payments right away.

A construction loan is designed to finance a home while it is being built. Instead of receiving all of the funds upfront, money is released in stages as construction progresses.

Another key difference is how the loan is secured. Traditional mortgages are backed by an existing home, while construction loans are secured by the projected value of the completed home. Because the lender is financing a home that has not yet been built, construction loans often involve additional reviews, inspections, and documentation.

The table below highlights some of the biggest differences:

| Construction Loan | Traditional Mortgage |

|---|---|

| Finances a home being built | Finances an existing home |

| Funds released in stages | Full loan amount provided at closing |

| Requires inspections during construction | No construction inspections required |

| Typically short-term during the build phase | Long-term financing |

| Often converts into a traditional mortgage after completion | Mortgage begins immediately |

For buyers, one of the biggest differences is how construction funds are distributed throughout the build. Rather than receiving the entire loan amount at once, lenders release funds in phases as key milestones are completed. This process is known as a draw schedule.

See the Consumer Financial Protection Bureau for additional resources about mortgages and home financing.

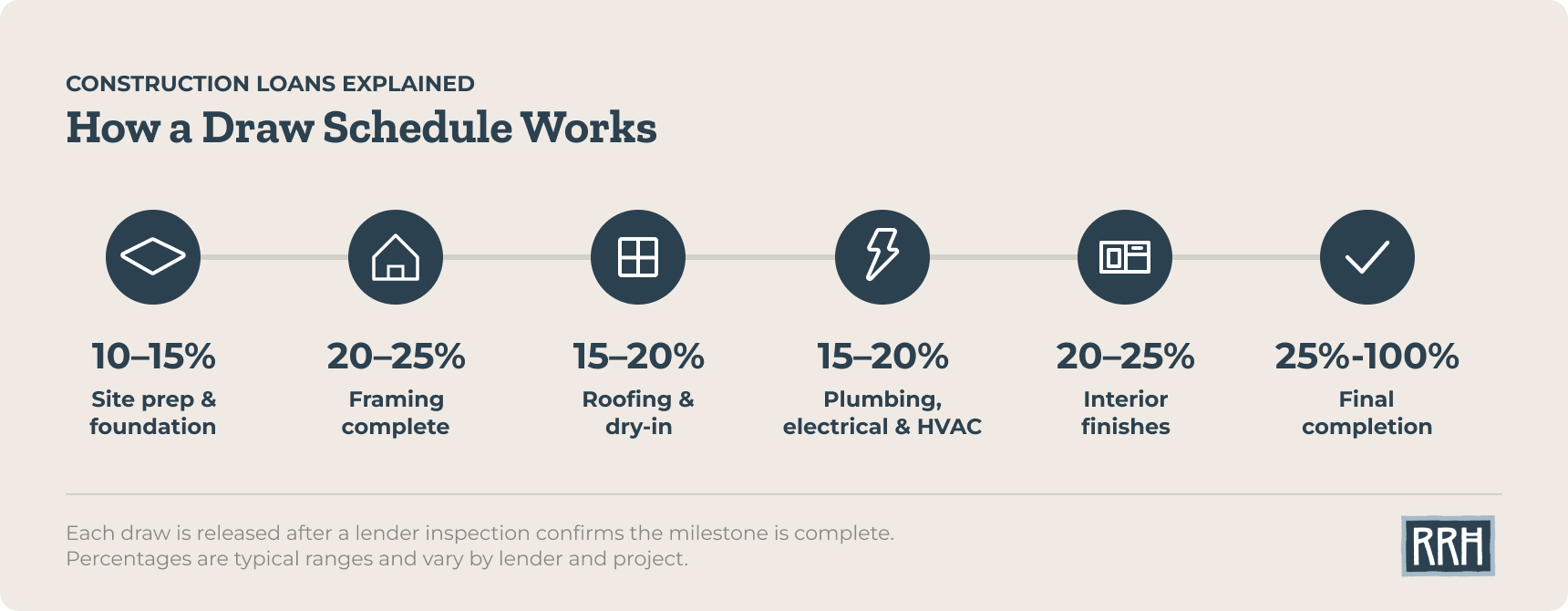

What is a draw schedule, and how does it work?

A draw schedule is the timeline lenders use to release construction funds throughout the building process. Instead of receiving the full loan amount upfront, lenders distribute money in phases as major milestones are completed.

A typical draw schedule may include draws at the following milestones:

- Site preparation and foundation

- Framing

- Roofing and dry-in

- Plumbing, electrical, and HVAC

- Interior finishes

- Final completion and Certificate of Occupancy

Before each draw is released, the lender typically sends an inspector to confirm the work has been completed.

During construction, borrowers usually pay interest on the amount that has already been released, not the total loan amount.

You can help prevent unnecessary delays and lender coordination issues by working with an experienced builder such as Rock River Homes when building throughout Virginia, the Northern Neck, and Northern North Carolina. Our team coordinates inspections, draw requests, and lender communication throughout the building process to help your project move efficiently.

Construction Loan Interest Rates

You may notice that construction loan interest rates are often higher than traditional mortgage rates because the lender is taking on more risk while financing a home that has not yet been completed.

In many cases:

- Construction loan rates are often higher than traditional mortgage rates.

- Rates are often variable during construction

- The final mortgage rate may differ depending on the loan structure and market conditions

If you’re building a home in Virginia or North Carolina, you can monitor mortgage trends through resources like Freddie Mac’s Primary Mortgage Market Survey. Because construction timelines can last several months, be sure to discuss rate lock options with your lender early in the process.

“With today’s market volatility, it is important for consumers to understand the opportunities available to lock in current interest rates during the construction process,” recommends Gary Collins, Director of Sales and Marketing.

Rock River Homes may be able to help simplify the financing process by handling the construction loan directly. In these situations:

- Buyers may avoid upfront construction loan closing costs

- Buyers may not make monthly payments during construction

- Buyers complete one closing after construction is finished

How much do you need for a down payment?

Most construction loans require a down payment between 10–20%, though requirements vary depending on the lender, loan type, credit profile, and whether land is already owned.

Some government-backed loan programs, such as FHA construction loans, may allow qualifying buyers to put down less. The Federal Housing Administration (FHA) provides additional information about FHA-backed loan programs.

If you already own land, the value built up in that property can often count toward your down payment.

Buyers building in rural areas throughout Virginia and Northern North Carolina may also qualify for certain USDA Rural Development loan programs depending on property eligibility. The USDA Property Eligibility Map allows buyers to explore eligible areas.

Own Land in Virginia or Northern North Carolina?

Your land equity may count toward your down payment. Buyers building on inherited or privately owned land are often able to reduce upfront construction financing costs using existing equity.

This is especially common for buyers in counties like Amelia, Powhatan, Goochland, Cumberland, Buckingham, Lancaster, Northumberland, Middlesex, and surrounding rural areas where inherited land and family property are more common.

For more information, be sure to see additional homebuyer resources available through Virginia Housing.

Construction-to-permanent Loans vs. Standalone Construction Loans

There are two primary types of construction loans that are important to understand when building a home:

- Construction-to-permanent loan: buyers typically complete one closing that transitions into their long-term mortgage after construction is complete.

- Standalone construction loan: buyers usually complete two separate closings: one for construction financing and another for the final mortgage.

Construction-to-permanent Loans

Also called a “one-time close” loan, this option converts automatically into a traditional mortgage once construction is complete.

Benefits often include:

- One closing

- One set of closing costs

- Simplified transition to permanent financing

This is one of the more common financing structures for custom home buyers.

Standalone Construction Loans

A standalone construction loan requires two separate closings:

- The construction loan

- The permanent mortgage after the home is complete

While this structure can provide flexibility, it often creates:

- Additional closing costs

- More lender coordination

- More documentation and approvals

- Potential exposure to changing interest rates during construction

RRH Builder-Managed Financing

In some situations, Rock River Homes may be able to finance the construction phase directly. Instead of requiring buyers to secure and manage a separate construction loan, RRH handles the construction financing throughout the build process.

This approach can simplify the homebuilding experience by reducing lender coordination, paperwork, and upfront costs that are often associated with traditional construction loans.

For qualifying buyers, benefits may include:

- No upfront construction loan closing costs

- No monthly payments during construction

- One closing after construction is complete

- Fewer administrative steps during construction

The comparison below highlights some of the key differences between common construction financing options.

Can you use a construction loan to buy land?

In many cases, you can also use a construction loan to purchase land. This allows buyers to combine land and construction into a single loan instead of securing them separately.

For buyers who already own land, that property may sometimes be used as collateral or applied toward the required down payment. This is especially common for buyers building in rural counties throughout Virginia and Northern North Carolina, including Lancaster, Northumberland, Buckingham, Amelia, and surrounding areas where family land ownership is more common.

Buyers should also factor in the hidden costs of buying land, including grading, wells, septic systems, permits, and utility connections, which may need to be included in the total project budget.

What do lenders look at to approve a construction loan?

Construction loan approval typically involves more documentation than a traditional mortgage because the lender is evaluating both the buyer and the construction project itself.

Lenders commonly review:

- Credit score

- Monthly debt compared to income

- Income and employment history

- Land ownership details

- Builder qualifications and licensing

- Construction plans and specifications

- Build timeline and contract pricing

For conventional construction loans, many lenders prefer credit scores of 680 or higher.

Construction lenders do not just evaluate the buyer. They also review the builder’s licensing, experience, insurance, and construction track record before approving the loan. Working with an established builder like Rock River Homes can help simplify the approval process because lenders are often more comfortable financing experienced, licensed builders with a proven track record.

Step-by-step Process to Get a Construction Loan

While every lender operates slightly differently, the construction loan process typically follows these steps:

- Get pre-qualified

Pre-qualification gives buyers an early estimate of budget, financing options, and expected monthly payments before moving too far into the building process. This should happen before signing a construction contract. - Choose your builder and finalize plans

Lenders typically require finalized home plans, specifications, pricing, and contracts before approving the loan. - Appraisal of the future home value

The lender orders an appraisal based on the projected value of the completed home. - Loan review and approval

The lender reviews financial documentation, project details, builder credentials, and appraisal information. - Loan closing

Construction financing is finalized and the project is ready to begin. - Construction begins

Funds are released in stages throughout construction according to the draw schedule.

One of the biggest mistakes buyers make is waiting too long to begin financing conversations. Getting pre-qualified early can help prevent major delays later in the process.

Common Mistakes Buyers Make with Construction Loans

Many construction loan issues can be avoided with early planning and realistic budgeting.

Some of the most common mistakes include:

- Waiting too long to get pre-qualified

- Underestimating site preparation costs

- Forgetting to budget for wells, septic systems, permits, or utilities

- Choosing a lender unfamiliar with rural construction projects

- Not understanding how rate changes can impact longer build timelines

- Assuming construction loans work like traditional mortgages

Choosing a lender unfamiliar with rural construction projects can create unnecessary delays during approvals and draw schedules.

Because Rock River Homes regularly builds throughout Virginia and Northern North Carolina, our team understands the unique challenges that can come with rural land development, including wells, septic systems, grading, permitting, and lender coordination.

How Rock River Homes Works with Lenders

Financing is one of the most important parts of the custom homebuilding process, and having the right partner matters.

Rock River Homes works with lenders familiar with construction financing across Virginia and Northern North Carolina, including rural and build-on-your-lot projects.

For qualifying buyers, Rock River Homes can also handle the construction financing directly, which may provide several advantages:

- No upfront construction loan closing costs

- No monthly payments during construction

- One closing after the home is complete

- Less paperwork and administrative stress

- Faster progress without repeated lender approvals

Our goal is to make the financing process feel clear, manageable, and predictable.

Applying your Construction Loan Knowledge

Construction loans can feel complicated at first, but understanding the basics early can help buyers make more informed decisions throughout the building process.

Understanding draw schedules, down payments, lender requirements, and types of financing can help you avoid delays and prepare more confidently for your build.

If you’re planning to build throughout Virginia or Northern North Carolina, early financing conversations are one of the smartest steps you can take.

Explore the Rock River Homes Financing page and How We Work page to learn more about the custom homebuilding process.

Common Questions About Construction Loans

Even after understanding the basics, many buyers still have practical questions about how the construction loan process works during a real build.

Do you make mortgage payments during construction?

With many traditional construction loans, borrowers make interest-only payments during the construction phase based on the amount already released from the loan.

However, when Rock River Homes handles the construction financing directly, buyers may not make monthly payments during construction. Instead, buyers complete one closing after the home is finished.

Can land count as a down payment for a construction loan?

In many cases, yes. If you already own land, the value built up in that property may count toward your required down payment.

This is especially common for buyers building on inherited family land or privately owned lots in areas like Amelia County, Lancaster County, Northumberland County, Powhatan County, and surrounding rural areas throughout Virginia and Northern North Carolina.

What credit score do you need for a construction loan?

Requirements vary by lender and loan type, but many conventional construction loans prefer a credit score of 680 or higher.

Lenders also evaluate:

- Monthly debt compared to income

- Income history

- Land ownership

- Construction plans

- Builder qualifications

What is the difference between a construction loan and a traditional mortgage?

A traditional mortgage provides funding for an existing home. A construction loan funds a home while it is being built and releases money gradually throughout the project.

Construction loans also involve:

- Draw schedules

- Inspections during construction

- Builder approval requirements

- Different loan review processes

What is a draw schedule in construction financing?

A draw schedule is the system lenders use to release funds throughout the building process as construction milestones are completed.

Typical draw stages include:

- Foundation

- Framing

- Roofing and dry-in

- Mechanical systems

- Interior finishes

- Final completion

Can you lock your interest rate before construction is complete?

Some lenders offer rate lock options for construction-to-permanent loans, though terms and availability vary.

What should you do before applying for a construction loan?

Before applying, buyers should:

- Review their budget and monthly payment goals

- Research land and site costs

- Gather income and financial documentation

- Speak with builders early

- Get pre-qualified before signing a construction contract

Early planning can help avoid delays and unexpected financing issues later in the project.

What costs are included in a construction loan?

Depending on the lender and loan structure, construction loans may include:

- Land purchase

- Site preparation

- Foundation work

- Construction labor and materials

- Wells and septic systems

- Utility connections

- Permits and inspections

If you are building a home in Virginia or North Carolina, it’s important to discuss the project scope early to ensure all major costs are included in the financing plan. Learn more about Hidden Costs on the Rock River Homes blog.

How long does it take to get approved for a construction loan?

Approval timelines vary by lender, but many buyers should plan for several weeks to complete pre-qualification, documentation review, appraisal, and final approval. Starting financing conversations early can help avoid delays once construction is ready to begin.

Become Part of the RRH Family

Explore the ways Rock River can help you find the perfect fit for you and your family.